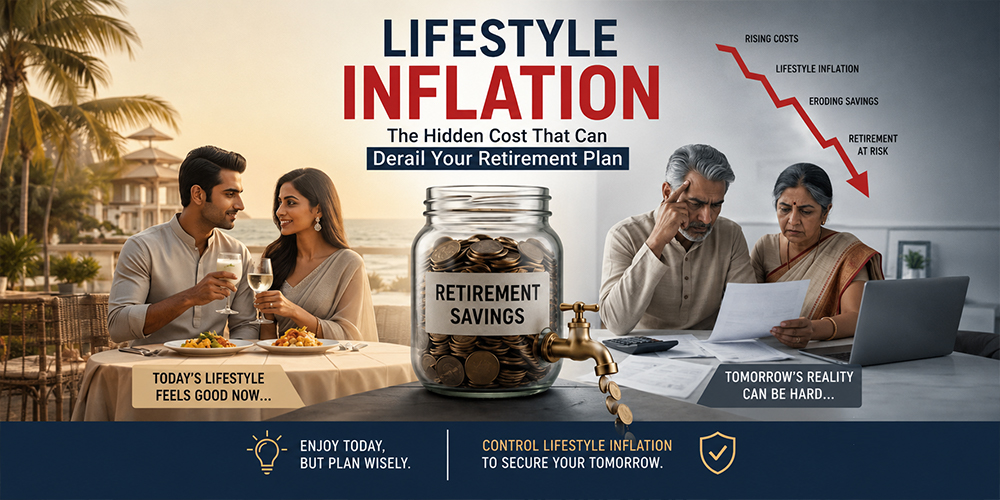

Lifestyle inflation is when your spending rises automatically as your income grows — and it poses a far greater threat to your retirement than official CPI inflation. Most retirement plans are built around a 5–6% inflation assumption. But if your actual lifestyle expenses are growing at 10–12% a year due to category upgrades and rising aspirations, your retirement corpus could fall short by crores. Here’s what lifestyle inflation is, how to spot it, and how to protect your retirement plan against it.

What Is Lifestyle Inflation?

Lifestyle inflation occurs when your personal cost of living rises faster than the official inflation rate — not because prices have increased, but because your preferences have changed.

As income grows, what once felt like a luxury gradually becomes a baseline expectation. A smartphone that cost ₹15,000 a decade ago has been replaced by a flagship device costing ₹60,000–₹80,000. The first family car was a hatchback at ₹5–6 lakh; today, first-time buyers often opt for SUVs at ₹12–15 lakh or more.

This is lifestyle inflation — and it’s entirely invisible to government CPI reports.

How Is Lifestyle Inflation Different from CPI Inflation?

The Consumer Price Index (CPI) and Wholesale Price Index (WPI) measure how the prices of a fixed basket of goods and services change over time. These are useful macroeconomic indicators, but they do not capture how your personal spending basket evolves.

Lifestyle inflation is driven by category upgrades — you don’t just pay more for the same product, you move to a higher category altogether.

Examples of category upgrades that drive lifestyle inflation:

- Motorcycles: A Himalayan 450 that cost ₹3.70 lakh in 2024 now costs approximately ₹4.10 lakh — an 11% rise. But when the time comes to upgrade, most riders don’t buy another Himalayan. They move to a premium adventure tourer. The actual spend increase? 50–100% or more.

- Cars: From a hatchback to an SUV to a luxury SUV. Each upgrade reflects lifestyle inflation, not just price inflation.

- Smartphones: The ₹15,000 phone of ten years ago has become the ₹80,000 flagship of today.

- Travel: Weekend drives become resort stays. Domestic holidays become international trips. Economy becomes business class.

- Dining: Occasional restaurant meals become regular fine-dining and weekly food delivery.

- Housing: A functional apartment evolves into a larger home in a premium locality with better amenities.

Each of these upgrades may be entirely justified. But they compound. And they make the 5–6% inflation assumption in most retirement calculators dangerously optimistic.

Why Does Lifestyle Inflation Matter for Retirement Planning?

The question retirement planning should answer is not “How much money will I need to survive?” It is: “How much money will I need to maintain the lifestyle I have built?”

These are very different numbers.

-

Lifestyle Creep Becomes Your New Normal

What once felt like a luxury — air conditioning, premium healthcare, international travel, high-end gadgets — eventually becomes an expectation. Retirement planning that ignores this drift will underestimate future expenses significantly.

-

Category Upgrades Shift Your Cost Base Permanently

Retirement calculators that apply only CPI inflation assume you will replace products with identical alternatives. In practice, people upgrade. The spending base that gets inflated forward is already elevated — and the inflation applied to it is often too low.

-

Healthcare Inflation Compounds the Problem

Medical inflation in India has historically grown faster than general CPI. As life expectancy increases, retirees face 25–35 years of healthcare expenses that may rise at 10–15% annually — well above the standard planning assumptions.

-

A Small Error in Inflation Assumptions Creates a Large Corpus Gap

Consider this comparison:

Assumption Current Annual Expenses Annual Expenses After 20 Years 6% Inflation ₹12,00,000 ₹38,00,000 10% Inflation ₹12,00,000 ₹80,00,000 The difference is more than ₹40 lakh per year — and that gap widens every year through retirement. A corpus designed for ₹38 lakh per year will run dry far sooner than expected if actual expenses are ₹80 lakh per year.

How to Protect Your Retirement Plan from Lifestyle Inflation

Define Your Future Lifestyle Concretely

- What kind of travel do you want in retirement?

- Will you upgrade your home or vehicle in the next 10 years?

- What healthcare standard do you expect — government hospitals or premium private care?

- What will family responsibilities look like — weddings, education, support for parents?

- What hobbies or passions do you plan to pursue?

Increase Investments Every Time Income Increases

The most effective habit against lifestyle inflation is a simple rule: whenever income rises, direct a meaningful portion of that increase toward investments before expanding lifestyle spending. This allows your wealth to grow alongside your lifestyle, rather than being consumed by it.

Use a Higher Inflation Rate in Your Retirement Calculations

Most financial planning software allows you to adjust the assumed inflation rate. If your lifestyle expenses are growing at 8–10% historically, use that figure rather than the CPI default of 5–6%. A slightly conservative assumption now is far better than a shortfall in retirement.

Review Your Financial Plan Regularly

A retirement plan prepared five years ago reflects your aspirations of five years ago. Life changes. Income changes. Goals change. A plan that is not reviewed becomes a plan that is wrong. Schedule a formal review of your retirement strategy at least every two years.

Invest for Real Returns That Outpace Lifestyle Inflation

Wealth preservation is not enough — your investments must outpace your personal rate of inflation, not just the CPI. This requires a long-term, growth-oriented investment strategy, ideally with professional guidance tailored to your specific lifestyle trajectory.

Questions to Ask Yourself Before Your Next Retirement Review

- Am I using CPI inflation or my actual lifestyle inflation rate in my retirement projections?

- Will my current investment returns outpace my personal spending growth over the next 20–30 years?

- Have I accounted for likely lifestyle upgrades — housing, travel, healthcare — in my corpus calculations?

- Is my retirement plan designed for survival or for the comfort I have worked to build?

- When did I last update my financial plan to reflect how my life and aspirations have changed?

Frequently Asked Questions About Lifestyle Inflation and Retirement

Lifestyle inflation is the tendency for personal spending to increase as income grows. Rather than saving or investing the additional income, people upgrade their standard of living — moving to more expensive categories of goods and services. Over time, this raises the personal cost of living faster than official inflation rates.

Most Indian retirement calculators assume an inflation rate of 5–6%, aligned with CPI. But if your actual lifestyle expenses are growing at 8–12% annually due to category upgrades, your retirement corpus estimate will be significantly understated. You may reach retirement with a corpus that feels large but is insufficient to sustain your actual lifestyle.

CPI measures price increases on a fixed basket of goods. Lifestyle inflation measures the change in your personal spending driven by changing preferences and category upgrades — spending more not because prices rose, but because your choices changed.

For most urban professionals, using 8–10% for lifestyle-related expenses and 10–15% for healthcare is more realistic than the standard 5–6%. The right rate depends on your specific spending history and lifestyle trajectory, which a Certified Financial Planner can help you assess.

Work with a financial planner to map your likely lifestyle in retirement — not just what you spend today. Review your plan every two years. Use a personal inflation rate based on your actual spending growth, not CPI. Increase investments alongside income increases, and invest for real returns that outpace your personal rate of inflation.

Yes — high earners are often most vulnerable to lifestyle inflation because their income growth enables significant lifestyle upgrades. Without deliberate planning, their spending base rises dramatically, making the retirement corpus needed far larger than assumed.

About the Author

Connect with Niraj Nanal for a personalised financial planning consultation.